In response to COVID-19, Packaging World magazine polled its readership of CPGs and brand owners to begin to see how the industry was dealing with the crisis. The poll, available here, is still open and still collecting data, but the following is an early snapshot of results.

The survey, sent out via email to a targeted audience on March 26, netted 115 highly qualified responses from food and beverage, healthcare, cosmetics, personal care, and other packaged goods manufacturers. Respondents ranged from engineers to package design and development, but the largest portion, at 26% of all responses, were CEOs or senior management.

62% of respondents are still coming into the office, with the remaining 38% working from home. It should be noted that the lion’s share of respondents (81%) come from the food and beverage industry, with others in healthcare packaging, so most respondents are deemed essential workers by the government.

An impressive 19% of respondents are either in the process of refitting or retooling, or considering doing so, in support of production to help governmental and health organizations with respirators, masks, or other critical healthcare materials relevant to suppressing the spread of COVID-19. On Friday, after the survey was sent to the Packaging World Audience, the White House said it would fully invoke the Defense Production Act, potentially compelling private businesses to produce essential healthcare materials. Still, 12% of survey respondents already are doing so, and another 7% are discussing doing so. Again, with 82% of respondents in the food and beverage industry, many are already deemed essential.

Major themes among write-in answers to the basic question: What is your company’s biggest challenge related to COVID-19? center around the following:

· Foodservice sector shutdown

· Exacerbated labor shortage with fears of sickness, school closures, etc.

· Sourcing materials and ingredients (China specifically)

A remarkable 55% of respondents say that supply chains have not been disrupted, at least not in the short term. One respondent added: “only a small portion of our supply chain is affected; some ingredient delays and sanitizer shortages,” and another said “Ingredients were initially the issue, but our carriers have since bounced back. Otherwise, it has been surprisingly good for us.”

In general, there have been some delays in materials and ingredient inputs, but respondents’ general tone is cautiously optimistic, according to the survey. The simplest, yet perhaps most poignant, response simply said “Basic needs are being met.”

However, there are those that are struggling to source raw materials, packaging materials especially. And despite the positive tone about how well the supply chain has held up so far, the future is less certain to respondents. When asked how they will keep up with business in the future if restrictions remain in place for more than 2-3 months, such stark responses as “May not survive” were entered on the survey. Those, though, are balanced by more optimistic, though pragmatic, answers. For instance, one respondent said: “As long as ingredients/materials continue to come in and our clients are still taking product away, we don't really see any issues with a longer restriction. The core issue would be the morale of our employees. 2-3 months is a long time to be under a shelter in place situation.”

The most representative and repeated (in spirit, at least) answer to the question about what the future holds was, “Do not know yet. Everything Is very fluid!”

Hiring and interviewing are split down the middle, with 49% of responding companies having such practices on hold, and the other 51% continuing on with personnel acquisition.

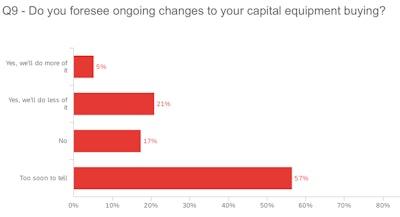

Nearly the same story can be told about capital expenditures—55% of respondents report that capital expenditures are on temporary hold, with the remaining 45% saying they’re continuing on as normal. The split division of answers in these two categories illustrates the lack of certainty or industry-wide agreement on what the future holds. Perhaps the clearest evidence of this is the majority of respondents, 57%, say that it’s too early to tell whether or not there will be any changes in capital equipment buying. Of the outliers to this opinion, 21% foresee limiting their capital expenditures, and 5% expect to expand them. And the remaining 17% foresee business-as-usual with regards to procuring equipment.

This survey will remain open and will be disseminated in the future to compare, apples to apples, responses during different collection points.