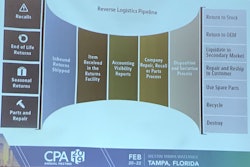

Speaking at the ProFood Tech Impact Zone on Wednesday, Carl Melville, Founder and CMO of the Melville Group, said that contract packagers used to be the “Rodney Dangerfield” of manufacturing – getting no respect. But all that has changed, as the decision to enter a relationship with a CP/CM usually originates at the C-suite or even the board level, and the service suites provided by CP/CMs continue to grow and create ever-evolving relationships.

Melville said the current CP/CM industry is valued at $59.8 billion, with an estimated value of $95.5 billion by 2022 and a CAGR of 12.24% over the next 5 years. Mergers and acquisitions are also a big part of this industry, at $5 billion dollars in 2018. Melville said one in four contract manufacturers are looking at acquiring, or being acquired, in the next year, and that more than half have 2 or more locations.

Brand cost cutting, or what Melville calls the “3G effect,” is driving this expansion to include CP/CM, by limiting R&D resources and internal innovations at a time when innovation is most needed. For the first time, category leaders are no longer dominating innovations. Over half of new products are coming from new companies, and 40% of the best-selling new products are from new companies, creating what Melville poses is a “massive risk” for established brands.

Other factors include digital transformation and the rise of premier store brands, which will “continue to disrupt traditional brand roles and increase margin pressures.”

There are four fundamental reasons to use a CP/CM:

- Efficiency – CP/CMs are offering a tighter focus on yields and productivity, and are making automation investments that allow more flexibility.

- Innovation – brands must innovate faster. CP/CMs are expanding to invest in R&D, pilot lines and labs and offering structured co-innovation programs. Partnering and collaborating with CP/CMs can increase level of product innovation for both brands and private labels.

- Speed-to-market – CP/CMs are assuming more responsibility in commercializing new products. Traditional brand speed-to-market often takes 18 months for a CPG, while a CP/CM is often able to offer a faster turn-around time.

- Capacity – CP/CMs are investing in automation, new lines and new locations, and also offer 24/7 run times. Melville said that CP/CMs are buying a lot of new equipment and opening new facilities right now.

Contract packagers and contract manufacturers must continue to evolve as well, says Melville. The pace of change will continue to accelerate.

Speaking at the ProFood Tech Impact Zone on Wednesday, Carl Melville, Founder and CMO of the Melville Group, said that contract packagers used to be the “Rodney Dangerfield” of manufacturing – getting no respect. But all that has changed, as the decision to enter a relationship with a CP/CM usually originates at the C-suite or even the board level, and the service suites provided by CP/CMs continue to grow and create ever-evolving relationships.

Melville said the current CP/CM industry is valued at $59.8 billion, with an estimated value of $95.5 billion by 2022 and a CAGR of 12.24% over the next 5 years. Mergers and acquisitions are also a big part of this industry, at $5 billion dollars in 2018. Melville said one in four contract manufacturers are looking at acquiring, or being acquired, in the next year, and that more than half have 2 or more locations.

Brand cost cutting, or what Melville calls the “3G effect,” is driving this expansion to include CP/CM, by limiting R&D resources and internal innovations at a time when innovation is most needed. For the first time, category leaders are no longer dominating innovations. Over half of new products are coming from new companies, and 40% of the best-selling new products are from new companies, creating what Melville poses is a “massive risk” for established brands.

Other factors include digital transformation and the rise of premier store brands, which will “continue to disrupt traditional brand roles and increase margin pressures.”

There are four fundamental reasons to use a CP/CM:

- Efficiency – CP/CMs are offering a tighter focus on yields and productivity, and are making automation investments that allow more flexibility.

- Innovation – brands must innovate faster. CP/CMs are expanding to invest in R&D, pilot lines and labs and offering structured co-innovation programs. Partnering and collaborating with CP/CMs can increase level of product innovation for both brands and private labels.

- Speed-to-market – CP/CMs are assuming more responsibility in commercializing new products. Traditional brand speed-to-market often takes 18 months for a CPG, while a CP/CM is often able to offer a faster turn-around time.

- Capacity – CP/CMs are investing in automation, new lines and new locations, and also offer 24/7 run times. Melville said that CP/CMs are buying a lot of new equipment and opening new facilities right now.

Contract packagers and contract manufacturers must continue to evolve as well, says Melville. The pace of change will continue to accelerate.

Speaking at the ProFood Tech Impact Zone on Wednesday, Carl Melville, Founder and CMO of the Melville Group, said that contract packagers used to be the “Rodney Dangerfield” of manufacturing – getting no respect. But all that has changed, as the decision to enter a relationship with a CP/CM usually originates at the C-suite or even the board level, and the service suites provided by CP/CMs continue to grow and create ever-evolving relationships.

Melville said the current CP/CM industry is valued at $59.8 billion, with an estimated value of $95.5 billion by 2022 and a CAGR of 12.24% over the next 5 years. Mergers and acquisitions are also a big part of this industry, at $5 billion dollars in 2018. Melville said one in four contract manufacturers are looking at acquiring, or being acquired, in the next year, and that more than half have 2 or more locations.

Brand cost cutting, or what Melville calls the “3G effect,” is driving this expansion to include CP/CM, by limiting R&D resources and internal innovations at a time when innovation is most needed. For the first time, category leaders are no longer dominating innovations. Over half of new products are coming from new companies, and 40% of the best-selling new products are from new companies, creating what Melville poses is a “massive risk” for established brands.

Other factors include digital transformation and the rise of premier store brands, which will “continue to disrupt traditional brand roles and increase margin pressures.”

There are four fundamental reasons to use a CP/CM:

- Efficiency – CP/CMs are offering a tighter focus on yields and productivity, and are making automation investments that allow more flexibility.

- Innovation – brands must innovate faster. CP/CMs are expanding to invest in R&D, pilot lines and labs and offering structured co-innovation programs. Partnering and collaborating with CP/CMs can increase level of product innovation for both brands and private labels.

- Speed-to-market – CP/CMs are assuming more responsibility in commercializing new products. Traditional brand speed-to-market often takes 18 months for a CPG, while a CP/CM is often able to offer a faster turn-around time.

- Capacity – CP/CMs are investing in automation, new lines and new locations, and also offer 24/7 run times. Melville said that CP/CMs are buying a lot of new equipment and opening new facilities right now.

Contract packagers and contract manufacturers must continue to evolve as well, says Melville. The pace of change will continue to accelerate.