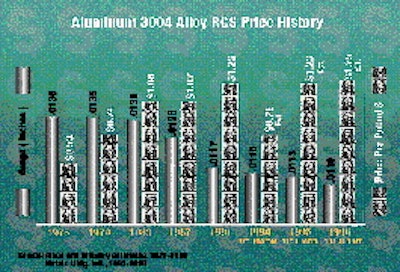

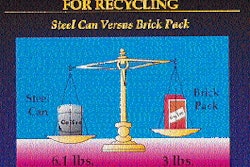

Could steel capture a noticeable share of the U.S. beverage can market in the next three years? Startling as it sounds, this worldwide trend may soon come to the U.S. It has its roots in the steady per capita increase in consumption of aluminum and the rising cost of the primary aluminum metal. The beverage can market has enjoyed tremendous growth over the past decade. Volume doubled from 52 billion cans in 1985 to 105 billion in '94. This year, however, this enormous market has been affected by price increases, particularly on aluminum cans, that went into effect in June '94. Pioneered by the new pricing formula announced by Alcoa (Pittsburgh, PA), the beverage industry could pay a premium of over $800 million this year to use aluminum instead of steel. Nevertheless, as of May, there are no reports of any canmaking lines in the U.S. being converted to steel production. Does this mean a total acceptance of the increase in aluminum sheet? Highly unlikely. For some indication of the bottlers' attitude, note recent overseas developments. In Europe over the last two to three years, aluminum has been repeating its U.S. performance, taking over one market after another: Greece, Italy, Scandinavia, and most recently, taking a majority of the United Kingdom market. However, in the words of aluminum specialist Robin Adams of Resource Strategies, "The aluminum price increase has totally stopped the European conversion." Several companies in three European markets have made decisions to change at least seven canmaking lines back to steel. On June 7, Carnaud Metalbox (Boulogne-sur-Se, France) and CCC Europe (Deventer, The Netherlands) both publicly announced the conversion of several lines from aluminum to steel. And there are rumors that similar changes are underway in Australia. If this is underway overseas, why not in the U.S.? How aluminum won market Today, almost 100% of beverage cans are made of aluminum. This year, an opportunity has arisen for steel to re-enter this market-one that until 30 years ago was exclusively the domain of steel. At that time, almost all beverage cans were three-piece soldered tinplate. Then two-piece drawn and wall-ironed aluminum cans appeared. Steel canmakers countered, first with welded and cemented three-piece cans, and later with a two-piece construction. Because the two-piece cans were preferred to three-piece and because of taste concerns, a large percentage of brewers considered aluminum technically superior. Throughout the '70s, steel battled aluminum for this market. With the advent of environmentalism and the energy crisis, aluminum had new allies in deposit legislation and in recycling. Because of the inherent value of recycled aluminum cans to aluminum companies, distributors and canners pressed makers for more aluminum cans to help cover collection and accounting costs in deposit states. And aluminum companies, led by Reynolds Metals (Richmond, VA) and Alcoa, created recycling programs that educated consumers that recycling aluminum cans back into new cans saved energy. For most of the '60s, '70s and '80s, the aluminum mills were forced to sell metal to the beverage canmakers at prices below their normal levels. That permitted their customers to match the costs of steel canmakers. As aluminum replaced steel cans in the market, the price of sheet rose. Offsetting this, canmaking technology similarly advanced, making possible the use of much lighter gauge aluminum. Table A shows canmakers' progress in lightweighting of beverage cans; Table B shows a 20-year trend in pricing. By last year, aluminum had all but vanquished steel from the soft drink market. At mid-year, the price of aluminum can sheet rose more than 50%. Almost overnight, soft drink canners faced a staggering increase in the cost of aluminum cans. Steel cans were no longer readily available, nor were plastic containers or glass considered a major alternative. So the soft drink industry entered 1995 negotiating for its requirements on a short-term basis, while recognizing that a major capital investment would be required to convert many canmakers back to steel. Consumer perceptions Any consideration of the re-emergence of the steel beverage can in the U.S. must take into account three factors: consumer perceptions, container performance and relative economics. In past years, it was often said that beer retained its flavor better when packaged in aluminum. This was due to reaction with iron in the steel. While true in theory and to the brewmaster's taste buds, the average consumer could rarely detect a difference. In any event, improved steel can coatings have largely overcome this problem. Today, most consumers consider any two-piece can to be aluminum. It's probable that the small percentage of steel beverage cans goes unnoticed by the public, unless they return cans to redemption centers. This practice, though, has largely been replaced by curbside collection, now accessible to some 45% of the U.S. population. The popularity of curbside recycling has led to the closing of many company-operated collection centers. In terms of performance, aluminum cans can be more sensitive to handling abuse than steel. Empty aluminum bodies, when conveyed on high-speed lines, are subject to more flange damage and denting. When filled with pressurized beverages and given adequate secondary packaging, aluminum cans obviously perform well. Steel can designers, recognizing that the beverage canners have adapted their handling systems for the thinner aluminum cans, are reducing the future starting gauges and sidewalls to achieve metal savings without losing all of their strength advantage. Steel cans have been at a disadvantage to aluminum because of the flavor sensitivity of certain beverages to iron. It has been necessary for steel cans to have heavier application weights of enamel inside coatings, usually through a double coat, to avoid excessive iron pick-up. Improvements in coatings and in application techniques have reduced this problem. But almost all steel beverage can lines incorporate extra trackwork and equipment to apply a second inside spray and bake cycle. Canner costs One of the largest single cost items for a beverage canner is the cost of the package itself, regardless of type. A small variation in the package cost can spell profit or loss in a beverage operation. Given similar market acceptance and package performance, the market shares of aluminum vs steel cans will be strongly influenced by comparative economics and availability. Although other factors played a big role in the past, today there may be little difference in container quality and performance. Thus production costs will be a strong factor in determining share for each material. In early 1994, it is estimated that the average production cost for 1ꯠ steel can bodies was approximately $1.06 higher than for 1ꯠ aluminum bodies. This year the comparison has drastically changed. The new pricing formula, based on the value of aluminum on the London Metals Exchange, shifted costs for can sheet from a basebox basis to a per-pound price. Because of rising costs of aluminum on the LME, the cost of body stock to a canmaker rose from a low of 78¢/lb in January '94 to a price of $1.23/lb a year later. As a commodity, aluminum metal, traded on the LME, is subject to fluctuations caused by world economic developments, political influences and speculation. These have caused wide shifts in the past decade, from a one-day high of over $2/lb in 1988 to a low of 47¢/lb in November '93. The tremendous '93-'94 price declines were largely caused by surplus aluminum stocks dumped on the market by Russia. For canmakers, raw materials, largely sheetstock, represent from 65 to 70% of the total production cost. Hence the consternation among canmakers and fillers when aluminum surged last year. And, of course, future costs will be subject to the fluctuations of the LME price, a factor that currently makes up almost 55% of the finished can body cost. The LME has always played a primary role in pricing for aluminum as well as for the tin cost in plated steel. While aluminum costs have soared, the price for steel tinplate for beverage cans has remained at the same level as in '94. This disparity is partially offset by lower coating and spoilage costs for aluminum canmakers, and the much higher scrap recovery value. Nevertheless, in '95, the aluminum beverage can body is almost $8/thousand or 22% higher than its steel counterpart. Despite this cost burden, as of mid-'95, not one company has converted a single line in the U.S. back to steel. Nor have any announcements been made about conversion. But it could be a serious mistake to assume there will be no changes in the next 12 months. Lightweighting ahead Steel mills, both overseas and in the U.S., are testing new lighter weight steel cans that will lessen their costs. At the same time, lightweighting continues to present cost savings for aluminum. However, given the higher wall strength of the current steel bodies, we believe the potential for lightweighting steel is greater than for aluminum. The most efficient body lines for aluminum in '96 will probably use 0.0110" gauge in place of 0.0112". Steel bodies will be made from 0.0077" gauge, double-reduced, in place of the current 0.0094" for an appreciable reduction in metal cost. On the other hand, the aluminum metal cost will decline only slightly, despite the gauge reduction because some experts anticipate increases in the price of primary aluminum on the LME. Thus, the cost gap between the two materials will widen. Table C illustrates the estimated bottom-line production costs of 12-oz beverage can bodies based on the specifications and metal costs in early '94, early '95 and with estimates for 1996. What had been a $1.06/thousand aluminum advantage in '94 could be changed to a huge $12.54/thousand premium by next year. Will the aluminum industry, canmakers and beverage companies allow aluminum can body prices to rise that high? Other than hedge buying, canmakers and the beverage industry will have few options. If primary metal prices climb, the aluminum companies are unlikely to discount much below the formula price (LME price per pound + conversion cost + Midwest delivery price). Even in Table C, the figures assume a market discount of 16% from the formula price that's based on existing discounts. Still, the aluminum body remains considerably more expensive than the steel body. We see two trends developing. The first is a resurgence of steel canmaking. Aluminum canmaking lines can be converted to production of steel bodies for an equipment investment that varies from $1 million to $3.5 million, depending on the current line configuration. With a savings of as much as $12/thousand, this investment in converting a line producing nearly a billion cans/yr would be recovered in less than three months. Can the steel industry handle a significant increased demand for tinplate? The change won't occur overnight. As canmakers announce conversions to steel, the mills will be easily capable of handling orders of up to 20 million additional baseboxes, or about 800ꯠ tons of steel. Even if, by chance, mill capacity is strained, canmakers will revert to their former practice of importing a portion of their needs. One overseas mill has already signaled its interest in renewing shipments to the U.S. The other trend, not to be dismissed lightly, is a growth in plastics in the beverage market. In '95, 20-oz bottles of polyethylene terephthalate (PET) have already exhibited more growth than any other beverage container. The use of 16-oz PET bottles is also increasing. And 12-oz PET bottles are on the horizon, having been test-marketed for more than a year. Although the economics and performance of this size is still being debated, the threat to cans from 16- and 20-oz PET bottles is very real. Today, it is only the lack of resin supply-and yes, the price-that holds back bottlers in '95. However, more resin capacity is coming onstream next year. It is anticipated that aluminum can costs will be even higher in '96 so as much as 5-10% of beverage canmaking capacity next year will be converted to steel, or in the process of conversion. And PET bottles will continue their intrusion into this lucrative packaging market.